The Weighted Average Cost of Capital is 9 and the Fcfs Are Expected to Continue Growing at a 5

What is the Weighted Average Cost of Capital (WACC)?

The weighted average cost of capital (WACC) is the average rate of return a company is expected to pay to all its shareholders, including debt holders, equity shareholders, and preferred equity shareholders. WACC Formula = [Cost of Equity * % of Equity] + [Cost of Debt * % of Debt * (1-Tax Rate)]

Table of contents

- What is the Weighted Average Cost of Capital (WACC)?

- Understanding WACC

- WACC Formula

- Market Value of Equity

- Market Value of Debt

- Cost of Equity

- Cost of Debt

- WACC Calculation – Basic Example

- WACC Calculation – Starbucks Example

- WACC Interpretation

- Limitations

- Sensitivity Analysis – WACC & Share Price

- In the final analysis

- WACC Video

- Recommended Articles

Understanding WACC

WACC is the weighted average of a company's debt and its equity cost. Weighted Average Cost of Capital analysis assumes that capital markets (both debt and equity) in any given industry require returns commensurate with the perceived riskiness of their investments. But does WACC help the investors decide whether to invest in a company or not?

To understand the Weighted Average Cost of Capital, let's take a simple example.

You can download this WACC Calculation - Excel Template here – WACC Calculation - Excel Template

Suppose you want to start a small business! You go to the bank and ask if you need a loan to start. A bank looks at your business plan and tells you that it will lend you the loan, but there is one thing that you need to do. Bank says that you need to pay 10% interest over and above the principal amount you borrow. You agree, and the bank lends you the loan.

You agreed to pay a fee (interest expense) to avail the loan. This "fee" is the "cost of capital" in simple terms.

As businesses need a lot of money to invest in expanding their products and processes, they need to source money. They source money from their shareholders in the form of Initial Public Offerings An initial public offering (IPO) occurs when a private company makes its shares available to the general public for the first time. IPO is a means of raising capital for companies by allowing them to trade their shares on the stock exchange. read more (IPO), and they also take a loan from banks or institutions. Companies need to pay the cost to have this large sum of money. We call this the cost of capital. If a firm has more than one source which they take funds from, we need to take a weighted average of the cost of capital

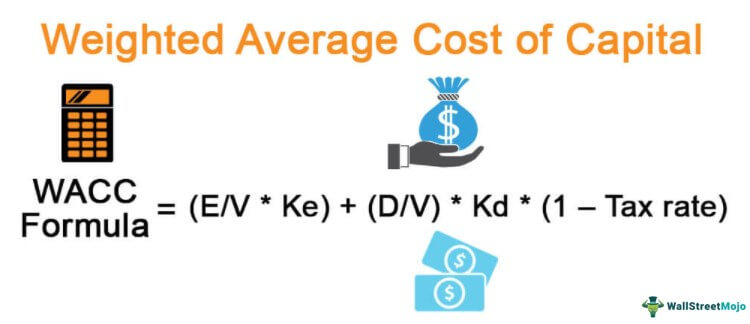

WACC Formula

Many investors don't calculate WACC because it's a little more complex than the other financial ratios Financial ratios are indications of a company's financial performance. There are several forms of financial ratios that indicate the company's results, financial risks, and operational efficiency, such as the liquidity ratio, asset turnover ratio, operating profitability ratios, business risk ratios, financial risk ratio, stability ratios, and so on. read more . But if you are one of those who would like to know how weighted average cost of capital (WACC) works, here's the formula for you.

WACC Formula = (E/V * Ke) + (D/V) * Kd * (1 – Tax rate)

You are free to use this image on your website, templates, etc, Please provide us with an attribution link Article Link to be Hyperlinked

For eg:

Source: Weighted Average Cost of Capital (WACC) (wallstreetmojo.com)

- E = Market Value of Equity

- V = Total market value of equity & debt

- Ke = Cost of Equity

- D = Market Value of Debt

- Kd = Cost of Debt

- Tax Rate = Corporate Tax Rate

The equation may look complex, but it will begin to make sense as we learn each term. Let's begin.

Market Value of Equity

Let's start with the E, the market value of equity. How should we calculate it? Here's how –

- Let's say Company A has outstanding shares of 10,000, and the market price of each of the shares at this moment is US $10 per share. So, the market value of equity would be = (outstanding shares of the Company A * market price of each share at this moment) = (10,000 * US $10) = US $100,000.

- The market value of equity can also be termed market capitalization. By using the market value of equity or market capitalization Market capitalization is the market value of a company's outstanding shares. It is computed as the product of the total number of outstanding shares and the price of each share. read more , investors can know where to invest their money and where they shouldn't.

Market Value of Debt

Now, let's understand the meaning of the market value of debt, D. How to calculate it?

- It's difficult to calculate the market value of debt because very few firms have their debt in outstanding bonds.

- We can directly take the listed price as the debt's market value if the bonds are listed.

- Now, let's go back to the Weighted Average Cost of Capital and look at V, the total market value of equity and debt. It is self-explanatory. We need to add the market value of equity and the estimated market value of debt, and that's it.

Cost of Equity

- Cost of Equity Cost of equity is the percentage of returns payable by the company to its equity shareholders on their holdings. It is a parameter for the investors to decide whether an investment is rewarding or not; else, they may shift to other opportunities with higher returns. read more (Ke) is calculated using the CAPM Model. Here's the formula for your reference.

- Cost of Equity = Risk-Free Rate of Return + Beta * (Market Rate of Return – Risk-free Rate of Return)

- Here, Beta = Measure of risk calculated as a regression of the company's stock price.

- The CAPM model was discussed extensively in another article CAPM Beta CAPM Beta is an essential theoretical measure of how a single stock moves with respect to the market. In this method, we determine the cost of equity by summing up the beta and risk premium product with the risk-free rate. read more . Please do have a look at it if you need more information.

Cost of Debt

- We can Calculate the cost of debt using the following formula – Cost of Debt = (Risk-Free Rate + Credit Spread) * (1 – Tax Rate)

- As the cost of debt (Kd) is affected by the tax rate, we consider the After-Tax Cost of Debt.

- Here, credit spread depends on the credit rating. Better credit rating will decrease the credit spread Credit Spread is the yield gap between similar bonds but with different credit quality. If a 5-year Treasury bond yields 5% and a 5-year Corporate Bond yields 6.5 percent, the gap over Treasury is 150 basis points (1.5 percent ). read more and vice versa.

- Alternatively, you can also take a simplified approach to calculating the Cost of Debt. You can find the cost of Debt as Interest Expense / Total Debt.

- Tax Rate is the Corporate Tax Rate, which is dependent on the Government. Also, note that if preferred stock is given, we also need to take into account the cost of preferred stock.

- If preferred stock is included, here would be the revised WACC formula – WACC = E/V * Ke + D/V * Kd * (1 – Tax Rate) + P/V * Kp. Here, V = E + D + P and Kp = Cost of Preferred Stocks

WACC Calculation – Basic Example

As there are so many complexities in WACC calculation, we will take one example each for calculating all the portions of the weighted average cost of capital. Then we will take one final example to ascertain the WACC.

You can download this WACC Calculation - Excel Template here – WACC Calculation - Excel Template

Let's get started.

Step # 1 – Calculating Market Value of Equity / Market Capitalization

Here are the details of Company A and Company B –

| In US $ | Company A | Company B |

|---|---|---|

| Outstanding Shares | 30000 | 50000 |

| Market Price of Shares | 100 | 90 |

In this case, we have been given both the numbers of outstanding shares and the market price of shares. So let's calculate the market capitalization of Company A and Company B.

| In US $ | Company A | Company B |

|---|---|---|

| Outstanding Shares (A) | 30000 | 50000 |

| Market Price of Shares (B) | 100 | 90 |

| Market Capitalization (A*B) | 3,000,000 | 4,500,000 |

Now we have the market value of equity or market capitalization of Company A and Company B.

Step # 2 – Finding Market Value of Debt

Let's say we have a company for which we know the total debt. Total Debt (T) = US $100 million. To find the market value of debt, we need to check if this debt is listed.

If yes, then we can directly pick the latest traded price. So, for example, if the trading value was $84.83 for a face value of $100, then the market value of debt will be $84.83 million.

Step # 3 Calculate Cost of Equity

- Risk Free Rate = 4%

- Risk Premium = 6%

- Beta of the stock is 1.5

Cost of Equity = Rf + (Rm-Rf) x Beta

Cost of Equity = 4% + 6% x 1.5 = 13%

Step # 4 – Calculate the Cost of Debt

Let's say we have been given the following information –

- Risk free rate = 4%.

- Credit Spread = 2%.

- Tax Rate = 35%.

Let's calculate the cost of debt.

Cost of Debt = (Risk Free Rate + Credit Spread) * (1 – Tax Rate)

Or, Kd = (0.04 + 0.02) * (1 – 0.35) = 0.039 = 3.9%.

Step # 5 – WACC Calculation

So after calculating everything, let's take another example of WACC calculation (weighted average cost of capital).

| In US $ | Company A | Company B |

|---|---|---|

| Market Value of Equity (E) | 300000 | 500000 |

| Market Value of Debt (D) | 200000 | 100000 |

| Cost of Equity (Re) | 4% | 5% |

| Cost of Debt (Rd) | 6% | 7% |

| Tax Rate (Tax) | 35% | 35% |

We need to calculate WACC for both of these companies.

Let's look at the WACC formula first –

WACC Formula = E/V * Ke + D/V * Kd * (1 – Tax)

Now, we will put the information for Company A,

weighted average cost of capital formula of Company A = 3/5 * 0.04 + 2/5 * 0.06 * 0.65 = 0.0396 = 3.96%.

WACC formula of Company B = 5/6 * 0.05 + 1/6 * 0.07 * 0.65 = 0.049 = 4.9%.

Now we can say that Company A has a lesser cost of capital (WACC) than Company B. Depending on the return both of these companies make at the end of the period, we would be able to understand whether, as investors, we should invest into these companies or not.

WACC Calculation – Starbucks Example

Assuming that you are comfortable with the basic WACC examples, let us take a practical example to calculate the WACC of Starbucks. Please note that Starbucks has no preferred shares A preferred share is a share that enjoys priority in receiving dividends compared to common stock. The dividend rate can be fixed or floating depending upon the terms of the issue. Also, preferred stockholders generally do not enjoy voting rights. However, their claims are discharged before the shares of common stockholders at the time of liquidation. read more and hence, the WACC formula to be used is as follows –

WACC Formula = E/V * Ke + D/V * Kd * (1 – Tax Rate)

Step 1 – Find the Market Value of Equity

Market Value of Equity = Number of shares outstanding x current price.

The market value of equity is also market capitalization. Let us look at the total number of shares of Starbucks –

source: Starbucks SEC Filings

source: Starbucks SEC Filings

- As we can see from above, the total number of outstanding shares is 1455.4 million

- Current Price of Starbucks (as of the close of December 13, 2016) = 59.31

- Market Value of Equity = 1455.4 x 59.31 = $86,319.8 million

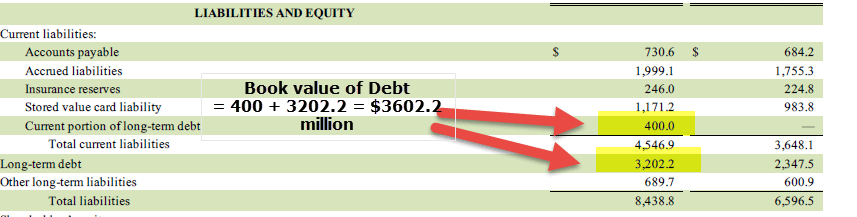

Step 2 – Find the Market Value of Debt

Let us look at the balance sheet of Starbucks below. As of FY2016, the book value of debt is current.

As of FY2016, book value of Debt is the current portion of long-term debt Current Portion of Long-Term Debt (CPLTD) is payable within the next year from the date of the balance sheet, and are separated from the long-term debt as they are to be paid within next year using the company's cash flows or by utilizing its current assets. read more ($400) + Long Term Debt ($3202.2) = $3602.2 million.

source: Starbucks SEC Filings

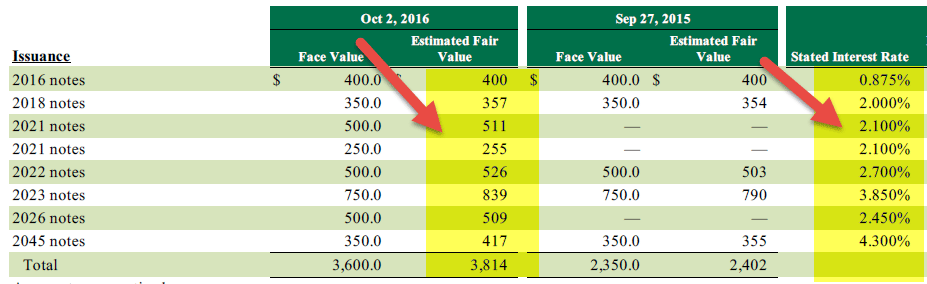

However, when we further read about Starbucks debt, we are additionally provided with the following information –

source: Starbucks SEC Filings

As we note above, Starbucks provides the fair value The fair value of an investment is the asset sale price that is agreeable to both the buyer and the seller. There is a caveat; the amount should be agreeable in a free trade scenario; there should be no external pressure or conditions. read more of the Debt ($3814 million) as well as the book value of debt The book value of debt is the total amount the company owes, which is recorded in the company's books. It is used in liquidity ratios compared to the company's total assets to check if the organization has enough support to overcome its debt. read more . Therefore, in this case, it is prudent to take the fair value of debt as a proxy for the market value of debt.

Step 3 – Find the Cost of Equity

As we saw earlier, we use the CAPM model to find the cost of equity Cost of Equity (Ke) is what shareholders expect for investing their equity into the firm. Cost of equity = Risk free rate of return + Beta * (market rate of return - risk free rate of return). read more .

Ke = Rf + (Rm – Rf) x Beta

Risk-Free Rate

Here, I have considered a 10-year Treasury Rate as the Risk-free rate. However, some analysts also take a 5-year treasury rate as the risk-free rate. Please check with your research analyst before taking a call on this.

source – bankrate.com

Each country has a different Equity Risk Premium. Equity Risk Premium primarily denotes the premium expected by the Equity Investor.

For the United States, Equity Risk Premium is 6.25%.

source – stern.nyu.edu

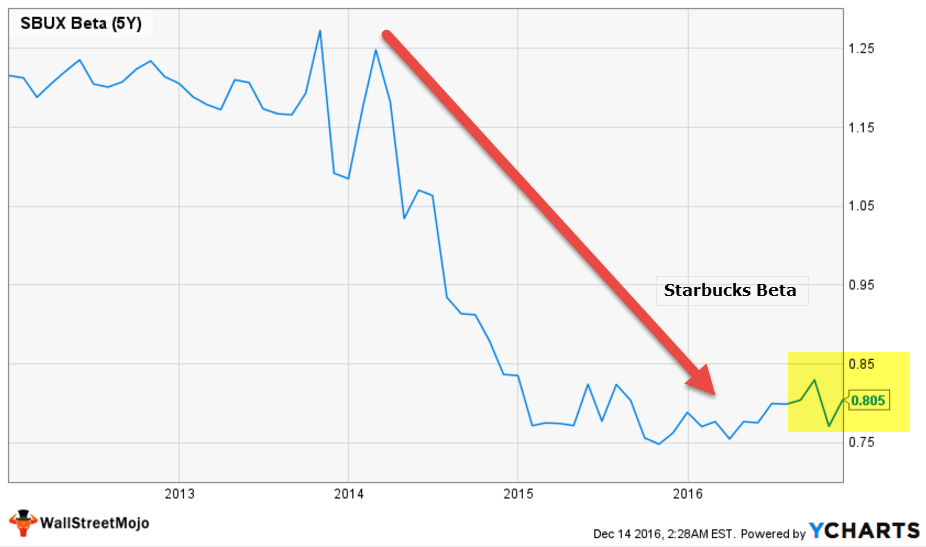

Beta

Let us now look at Starbucks Beta Trends over the past few years. The beta of Starbucks has decreased over the past five years. This means that Starbucks stocks are less volatile as compared to the stock market.

We note that the Beta of Starbucks is at 0.805x

With this, we have all the necessary information to calculate the cost of equity.

Cost of Equity = Ke = Rf + (Rm – Rf) x Beta

Ke = 2.47% + 6.25% x 0.805

Cost of Equity = 7.50%

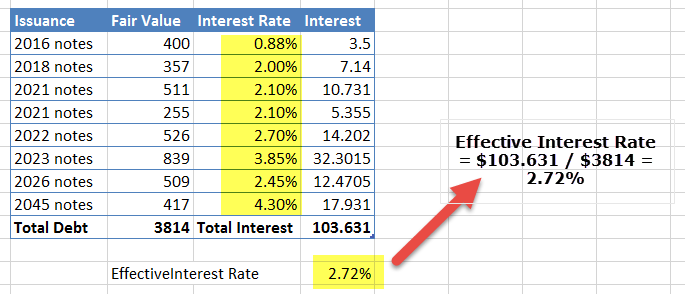

Step 4 – Find the Cost of Debt

Let us revisit the table we used for the fair value of debt. We are additionally provided with its stated interest rate.

Using the interest rate and fair value, we can find the weighted average interest rate of the total fair value of Debt ($3,814 million)

Effective Interest Rate Effective Interest Rate, also called Annual Equivalent Rate, is the actual rate of interest that a person pays or earns on a financial instrument by considering the compounding interest over a given period. read more = $103.631/$3,814 = 2.72%

Step 5 – Find the Tax Rate

We can easily find the effective tax rate Effective tax rate determines the average taxation rate for a corporation or an individual. For both, there is a similar formula only with variation in considering variables. The effective tax rate formula for corporation = Total tax expense / EBT read more from the Income Statement of Starbucks.

Please see below the snapshot of its income statement The income statement is one of the company's financial reports that summarizes all of the company's revenues and expenses over time in order to determine the company's profit or loss and measure its business activity over time based on user requirements. read more .

For FY2016, Effective tax rate = $1,379.7 / $4,198.6 = 32.9%

Step 6 – Calculate the weighted average cost of capital (WACC) of Starbucks

We have collected all the information that is needed to calculate WACC.

- Market Value of Equity = $86,319.8 million

- Market Value of Debt (Fair Value of Debt) = $3814 million

- Cost of Equity = 7.50%

- Cost of Debt = 2.72%

- Tax rate = 32.9%

WACC Formula = E/V * Ke + D/V * Kd * (1 – Tax Rate)

= (86,319.8/90133.8) x 7.50% + (3814/90133.8) x 2.72% x (1-0.329)

= 7.26%

WACC Interpretation

The interpretation depends on the company's return at the end of the period. If the company's return is far more than the Weighted Average Cost of Capital, then the company is doing pretty well. But if there is a slight profit or no profit, the investors need to think twice before investing in the company.

Here is another thing you need to consider as an investor. If you want to calculate the Weighted Average Cost of Capital, there are two ways you can use. The first is the book value, and the second is the market value approach.

As you can see that if you consider the calculation using market value, it's far more complex than any other ratio calculation; you can skip and decide to find the weighted average cost Average cost refers to the per-unit cost of production, calculated by dividing the total production cost by the total number of units produced. In other words, it measures the amount of money that the business has to spend to produce each unit of output. read more of capital (WACC) on the book value given by the company in their Income statement and in the Balance Sheet A balance sheet is one of the financial statements of a company that presents the shareholders' equity, liabilities, and assets of the company at a specific point in time. It is based on the accounting equation that states that the sum of the total liabilities and the owner's capital equals the total assets of the company. read more . But book value calculation is not as accurate as the market value calculation. And in most cases, market value is considered for the Weighted Average Cost of Capital (WACC) calculation for the company.

Limitations

- It assumes that there would be no change in the capital structure, which isn't possible all over the years, and if there is any need to source more funds.

- It also assumes that there would be no change in the risk profile A risk profile is a portrayal of the risk appetite of an investor. It is done by assessing an individual's capacity, interest, and willingness to take and manage risks. Preparing it helps financial advisors to assist clients in making effective investment decisions. read more . As a result of faulty assumption, there is a chance of accepting bad projects and rejecting good projects.

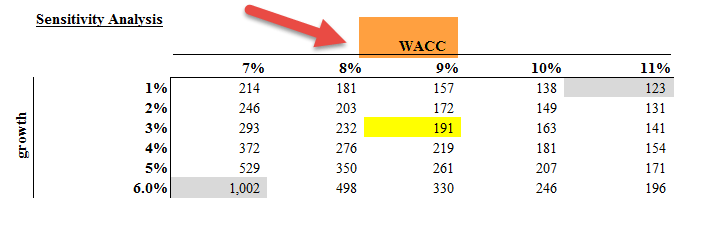

WACC is widely used in Discounted Cash Flow Valuation Discounted cash flow analysis is a method of analyzing the present value of a company, investment, or cash flow by adjusting future cash flows to the time value of money. This analysis assesses the present fair value of assets, projects, or companies by taking into account many factors such as inflation, risk, and cost of capital, as well as analyzing the company's future performance. read more . As an analyst, we do try to perform sensitivity analysis in Excel Sensitivity analysis in excel helps us study the uncertainty in the output of the model with the changes in the input variables. It primarily does stress testing of our modeled assumptions and leads to value-added insights. In the context of DCF valuation, Sensitivity Analysis in excel is especially useful in finance for modeling share price or valuation sensitivity to assumptions like growth rates or cost of capital. read more to understand the fair value impact along with changes in WACC and growth rate.

Below is the Sensitivity Analysis of Alibaba IPO Valuation Alibaba is the most profitable Chinese e-commerce company and its IPO is a big deal due to its size. With its huge size and network, Alibaba IPO may look at international expansion beyond China and may lead to price wars and intensive competition in the US. read more with two variables weighted average cost of capital (WACC) and growth rate.

Some of the observations that can be made about WACC –

- Fair valuation of stock is inversely proportional to the WACC.

- As the Weighted Average Cost of Capital increases, the fair valuation dramatically decreases.

- At the growth rate of 1% and the WACC of 7%, Alibaba Fair's valuation was $214 billion. However, when we changed the WACC to 11%, Alibaba's fair valuation dropped by almost 45% to $123 billion.

- This implies that fair valuation is extremely sensitive to the weighted average cost of capital (WACC), and one should take extra precautions to calculate WACC correctly.

In the final analysis

WACC is very useful if we can deal with the above limitations. It is exhaustively used to find the DCF valuation of the company. However, WACC is a bit complex and needs a financial understanding to calculate the Weighted Average Cost of capital accurately. Only depending on WACC to decide whether to invest in a company or not is a wrong idea. Investors should also check out other valuation ratios to make the final decision.

WACC Video

Recommended Articles

This article has been a complete guide to WACC, formula, its interpretation, and the weighted average cost of capital examples. Here we also calculated the WACC of Starbucks and discussed its limitations and sensitivity analysis. You may also have at these articles below to learn more about valuations –

- Calculate WACC

- FCFE Formula

- What is Cost of Equity?

Source: https://www.wallstreetmojo.com/weighted-average-cost-capital-wacc/

0 Response to "The Weighted Average Cost of Capital is 9 and the Fcfs Are Expected to Continue Growing at a 5"

Post a Comment